May 20, 2025

Invoice Factoring vs Bank Loans: Which Financing Option Is Right for Your Business?

When your business needs funding, two of the most common options are invoice factoring and bank loans. While both can provide working capital, they operate in very different ways, and choosing the right one can have a big impact on your cash flow, credit and flexibility.

In this guide, we’ll break down the differences between invoice factoring vs bank loans, explain how each option works and help you decide which financing solution best fits your business needs.

What Is Invoice Factoring?

Invoice factoring is a form of alternative funding that allows businesses to turn their unpaid invoices into immediate cash. Instead of waiting 30, 60 or even 90 days for customers to pay, companies sell their outstanding invoices to a third-party factoring company (also called a “factor”) in exchange for a cash advance.

Unlike a traditional loan, invoice factoring doesn’t create debt or require monthly repayments. Instead, it accelerates access to money your business has already earned, improving cash flow without taking on new liabilities.

This makes invoice factoring especially useful for businesses with consistent invoicing but long payment cycles, such as those in industries like construction, manufacturing or B2B services.

How Does Invoice Factoring Work?

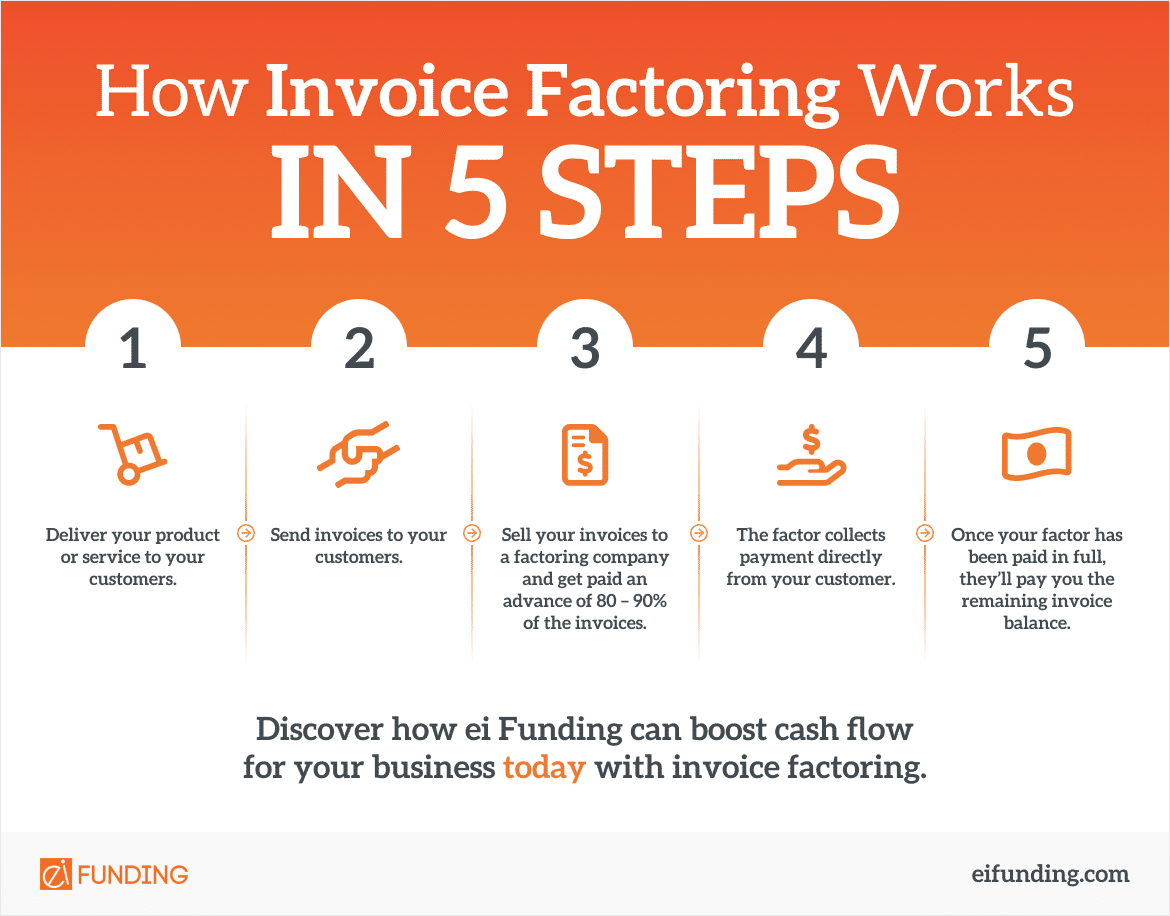

The invoice factoring process is straightforward and typically much faster than applying for a loan. Here’s how it works:

- You send an invoice to your customer for completed goods or services.

- You sell that invoice to a factoring company, which advances you up to 80-90% of its value.

- The factoring company collects payment directly from your customer.

- Once the invoice is paid, the factor sends you the remaining balance minus a small fee.

This funding can happen in just a few days, giving you quick access to working capital to cover payroll, purchase materials or take on new projects. And because repayment comes from your customers (not you), factoring is often easier to qualify for than traditional financing.

What Is a Business Bank Loan?

A business bank loan is a traditional form of financing where a bank lends your business a set amount of money that you repay over time with interest. Loans may be secured (backed by collateral) or unsecured (based on your creditworthiness), and they typically involve a formal application and underwriting process.

Once approved, you’ll receive a lump sum of capital and agree to fixed monthly payments over a specified term, often several years. Interest rates are generally lower than alternative lending options, but the process can take weeks, and approval depends heavily on your credit score, business history and available assets.

Bank loans can be a good option for businesses with strong financials and long-term funding needs, but they may not be ideal for companies that need fast cash or don’t qualify for traditional credit.

Invoice Factoring vs Bank Loans: Key Differences

| Feature | Invoice Factoring | Bank Loan |

| Funding Speed | Fast; typically 1-3 business days after approval | Slow; approval and disbursement can take weeks |

| Qualification Criteria | Based on your customers’ credit and invoice volume | Based on your business credit, collateral and financial history |

| Debt Incurred | No; you’re selling receivables | Yes; adds a new liability to your balance sheet |

| Repayment | Paid by your customers directly to the factoring company | Repaid in monthly installments by your business |

| Use of Funds | Flexible; use for payroll, operations, growth, etc. | Also flexible; often used for expansion, equipment or real estate |

| Cost Structure | Fees typically range from 1-5% of invoice value | Interest rates vary but may be lower than factoring fees |

| Best For | Businesses with slow-paying customers or limited credit history | Businesses with strong credit and long-term capital needs |

| Cash Flow Impact | Improves short-term cash flow without taking on debt | Can strain cash flow due to fixed monthly payments |

Invoice Factoring Pros and Cons

Pros of Invoice Factoring

- Fast Access to Working Capital: Most businesses receive funds within 1-3 days, much faster than the weeks-long wait for a traditional loan.

- No New Debt: Unlike loans, factoring doesn’t incur debt; you’re essentially selling your outstanding invoices at a discount.

- Easier Approval Process: Approval is based primarily on your customers’ creditworthiness, not your business’s credit history, making it ideal for businesses with less established credit histories.

- Flexible and Scalable: You choose which invoices to factor and when, allowing your financing to grow with your sales volume.

- Reduced Administrative Work: The factoring company handles collections, helping you save time and resources.

Cons of Invoice Factoring

- May Cost More Than Traditional Loans: Factoring fees typically range from 1% to 5% of the invoice value. While you’re not paying interest, the cost of invoice factoring can be higher overall if your customers take longer to pay.

- Customer Credit Risk: Your ability to get funded (and how much) depends on your customers’ payment behavior. If they pay late or default, your funding may be affected.

- Limited Use Cases: Invoice factoring only works for businesses that generate invoices. If you run a retail shop or rely on cash sales, it’s not a viable option.

Traditional Business Loan Pros and Cons

Pros of Bank Loans

- Lower Interest Rates: Traditional bank loans often offer lower interest rates than alternative financing options like invoice factoring, making them a cost-effective choice over time.

- Predictable Repayment Structure: With fixed interest rates, businesses can plan their finances around regular, predictable payment schedules.

- Helps Build Business Credit: Successfully managing a bank loan can improve your credit score, potentially opening doors to more favorable financing in the future.

- Large Loan Amounts Available: For well-qualified businesses, banks can offer access to substantial funding that may not be available through short-term lending options.

Cons of Bank Loans

- Slow Funding Timeline: The application and underwriting process can take several weeks, much longer than the 1-3 day turnaround of invoice factoring.

- Strict Eligibility Requirements: Banks often require a high credit score, strong financials and substantial collateral, making loans difficult to access for newer or smaller businesses.

- Inflexible Terms: Once approved, bank loan terms are fixed. If your business needs change, it may be difficult or costly to restructure the loan.

- Adds to Your Debt Load: Bank loans increase your liabilities and must be repaid on a set schedule, regardless of how your cash flow fluctuates.

Learn more about the pros and cons of bank loans →

When To Choose Invoice Factoring Over a Bank Loan

While both options can provide valuable funding, invoice factoring is often the better choice for businesses that need fast access to cash or don’t meet traditional lending requirements.

You might consider invoice factoring if:

- You have slow-paying customers and need to bridge cash flow gaps between invoicing and payment

- You need funding quickly — invoice factoring can be approved and funded in just a few days

- You want to avoid taking on new debt and prefer a financing solution that doesn’t affect your credit profile

- You’ve been denied a bank loan due to limited credit history or a lack of collateral

- Your business is growing, and you need scalable funding that can grow with your accounts receivable

For businesses with strong credit, stable revenue and the time to go through the application process, a traditional bank loan may be a good fit, especially for large, long-term investments.

But for companies looking for alternative funding options, especially those in industries like construction, manufacturing or staffing services, invoice factoring can offer a faster, more flexible path to working capital.

Additional FAQs: Invoice Factoring vs Bank Loans

Which is better for small businesses — invoice factoring or a bank loan?

It depends on your business’s needs and financial profile. Invoice factoring is often better for small businesses that need to boost their cash flow or have trouble qualifying for loans due to limited credit. Bank loans may offer lower interest rates but require more documentation and take longer to process.

Can you use invoice factoring and a bank loan at the same time?

Yes, it’s possible to use both, as long as your bank loan terms don’t restrict you from assigning receivables to a third party. Some businesses use invoice factoring for short-term cash flow needs while maintaining a long-term loan for larger investments.

What’s faster: invoice factoring or a bank loan?

Invoice factoring is much faster. Most businesses receive funding within 1 to 3 days after approval. In contrast, bank loans often require weeks of paperwork, underwriting and credit checks before funds are disbursed.

Does invoice factoring affect your credit score?

No, since invoice factoring is not a loan, it doesn’t show up on your business credit report or impact your credit score. That said, consistently using factoring responsibly can help stabilize cash flow and improve your financial position overall.

Are there industries where invoice factoring works better than loans?

Yes. Industries with long billing cycles and B2B customers like construction, manufacturing, healthcare, staffing and logistics are especially well-suited for invoice factoring. Businesses in these sectors often face cash flow gaps that factoring can quickly resolve.

Choosing the Right Financing Option for Your Business

When weighing invoice factoring vs bank loans, the best financing option depends on your business’s unique circumstances. If you have strong credit, collateral and time to wait, a traditional loan may offer long-term value at a lower cost.

But if your business needs fast funding, flexible terms and a way to unlock cash tied up in unpaid invoices, invoice factoring can be the smarter, more accessible solution. It’s especially useful for newer businesses, those with B2B customers or companies facing cash flow challenges.

Still unsure which is right for you?

Take our quick quiz to find out if invoice factoring is a good fit — or apply now and get funded in just a few days.

SHARE :

Ernane Iung is a seasoned C-suite executive with a 28-year dynamic career across four continents, including two decades in São Paulo, Brazil, where he held key roles with renowned multinationals such as GE, Whirlpool, Philips and Oster.

{kind=link}

{kind=link}

{kind=link}